미국 다우존스지수(DJIA, 다우지수)가 8,616p로 +256p, 3.07% 상승하였습니다.

원인은 '엠파이어 스테이트 제조업 지수'(Empire State Manufacturing Index)가 예상보다 큰 폭으로 호조세를 보였기 때문입니다.

엠파이어 스테이트 제조업 지수 _09.07.15, 양(+)전환 임박?

엠파이어 스테이트 제조업 지수(이하, '엠파이어 지수')는 -0.55를 기록하며, 수치가 양(+)전환에 임박한 징후를 보이고 있습니다.

엠파이어 스테이트 지수, 예상치와 실제 수치 _09.07.15 (현지)

2007년부터 2009년 상반기까지 약 2년 동안 최근 '엠파이어 스테이트 제조업 지수' 동향을 보면, 양전환한 경우가 드물었고, 2008년 중반 금융위기의 클라이막스를 계기로 1년 가까이 마이너스(-) 추세로 바닥을 기어왔음을 볼 수 있습니다.

엠파이어 지수는 6월달에 재차 하락하며, 다우존스 지수에 충격을 주기도 했으나,

7월 15일 발표 지표에서는 회복 추세가 유지되며, 양전환이 임박해 보이는 모습입니다.

엠파이어 스테이트 제조업 지수는

소비, 고용, 투자 등 미래 경제활동의 전망을 위한 선행 경기지표로 활용되고 있습니다.

엠파이어 스테이트 제조업 지수(Empire State Manufacturing Index)는 New York주 지역의

약 200개 제조업체에 대한 체감경기에 대한 조사치를 합산하여 발표됩니다.

엠파이어 지수는 월간으로 발표되는데, 저번달 6월 지수의 경우 지표가 좋지 않았기 때문에, 다우지수 기준 -187p, 2.13%의 하락을 이끌며 시장에 충격을 준 바 있습니다. 당시 다우존스 지수의 종가는 8,612p 였습니다.

(관련글, 2009.06.16 엠파이어스테이트제조업지수 발표내용, 다우존스지수)

반면에 7월 엠파이어 지수는 호조를 보였기 때문에, 다우존스 8,616p로 +256p, 3.07% 당일 급등을 이끌었습니다.

즉, 저번달과 정반대의 현상이 나타났다고 볼 수 있습니다.

그러나 다우존스 지수의 절대 수치로 보면, 저번달 지표 발표 직후 8,612p에서 이번달 8,616p로 +4p, 원점 수준으로 복귀한 것에 불과합니다. 즉, 증시는 대체로 경기지표 따라서 움직이는 것이죠.

한편, 미국경기가 2년여간의 바닥을 뒤로하고, 유력한 선행경기지표, 산업지표인 '엠파이어 제조업 지수'가 상승 전환을 임박한 모습을 보이고 있으므로, 기술적으로 이런 추세가 실제로 확연해 질 경우,

2009년 하반기에 미국 다우존스 지수는 연봉(Year Bar)으로 양봉을 시도할 가능성도 열려는 있습니다.

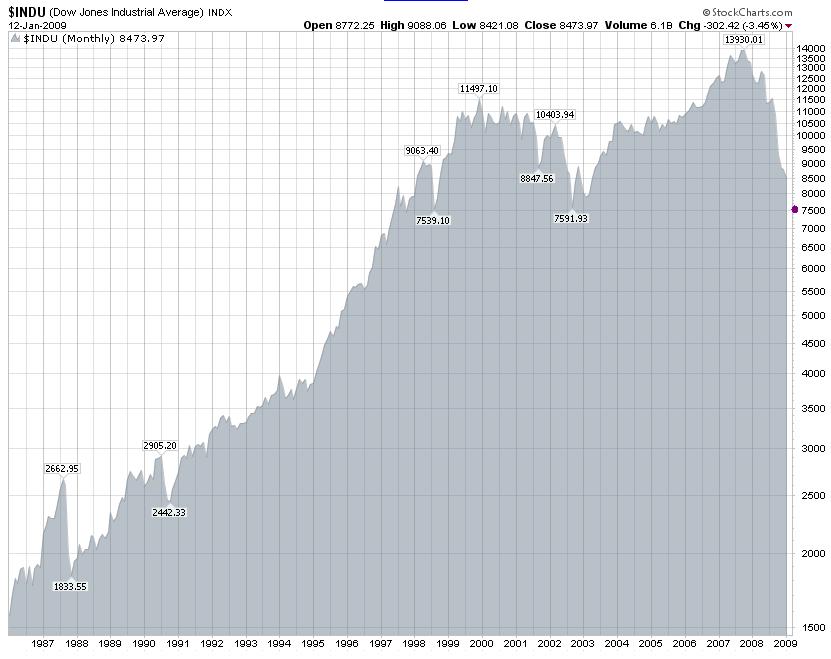

2009년 다우존스의 시초가는 약 9,000p 부근이었습니다.

다우존스, 나스닥 지수 _09.07.15 (현지)

|

Empire State Manufacturing Survey |

| |

| The monthly survey of manufacturers in New York State conducted by the Federal Reserve Bank of New York. |

|

July 2009 Report

Survey Indicators

Seasonally Adjusted

The Empire State Manufacturing Survey indicates that conditions for New York manufacturers were flat in July. The general business conditions index increased to a level close to zero, rising 9 points, to -0.6. The new orders index rose above zero for the first time in several months, and the shipments index also climbed into positive territory. The inventories index slipped to a record-low -36.5. The prices paid index rose above zero for the first time since November, while the prices received index held below zero. Employment indexes remained well below zero. Future indexes continued to be relatively optimistic about the six-month outlook, but were somewhat less buoyant than in June. The capital spending index fell several points, but remained above zero.

In a series of supplementary questions (see Supplemental Report tab), the median respondent indicated that total sales had fallen 15 percent from the first half of 2008 to the first half of 2009, and that the number of employees had decreased 10 percent. Declines for the full year were expected to be of the same respective magnitudes. The same questions were asked in July 2008; in that survey, sales had been seen as rising 5 percent, with employment levels being little changed. When asked if they had recently modified their production plans for the second half of 2009, close to 63 percent of respondents reported that they had scaled back plans, while just 21 percent indicated that they had increased them. This result reflects a much more negative assessment than what was reported in last July’s survey. In response to an additional set of questions new to this survey, manufacturers generally reported little effect thus far from the economic stimulus package.

General Business Conditions Index Rises, Holds around Zero

The general business conditions index rose several points in July, hovering around zero for the first time since last summer, at -0.6—suggesting that conditions neither worsened nor improved over the month. Twenty-three percent observed that conditions improved, less than the 28 percent reporting so in June, while 24 percent said that conditions worsened, well below the 38 percent who saw deteriorating conditions in June. The new orders index rose above zero for the first time since September 2008, climbing from -8.2 to 5.9. The shipments index rose similarly, from -4.8 to 11.0, its highest level in a year. The unfilled orders index held steady at -12.5. The delivery time index fell 4 points, to

-14.6, and the inventories index declined 11 points, to -36.5, a record low.

Input Prices Resume Increase

After several months of readings below zero, the prices paid index rose 16 points, to 10.4, the first positive value since November 2008, indicating that input prices are once again on the upswing. The prices received index remained negative, inching up 4points, to -8.3. Employment indexes remained negative and near June readings. The number of employees index was -20.8, and the average workweek index was -19.8.

Outlook Remains Favorable

The six-month outlook remained favorable in July, although future indexes were somewhat lower than last month. The future general business conditions index fell 14 points, but at 34.0 was well above the very low levels of earlier this year. The future new orders and shipments indexes also declined similarly. The future prices paid index rose 16 points, to 26.0, while the future prices received index held just below zero. Future employment indexes were positive. The capital expenditures index slipped 9 points, to 2.1, while the technology spending index held steady at 1.0.

(출처 :

Federal Reserve Bank of New York, 뉴욕연방은행)

엠파이어 스테이트 제조업 지수 발표에 따른 다우존스 지수 영향, 2009년 6월15일, 7월15일 (현지)

[관련글]

미국 기업재고, Business Inventories 월간 -1.0% 감소 _09.07.15

미국 내구재 주문, Durable Goods Orders 1.8% 개선 _09.06.24

미국 엠파이어 스테이트 제조업 지수 _09.06.16

sjcu0909.pdf

sjcu0909.pdf