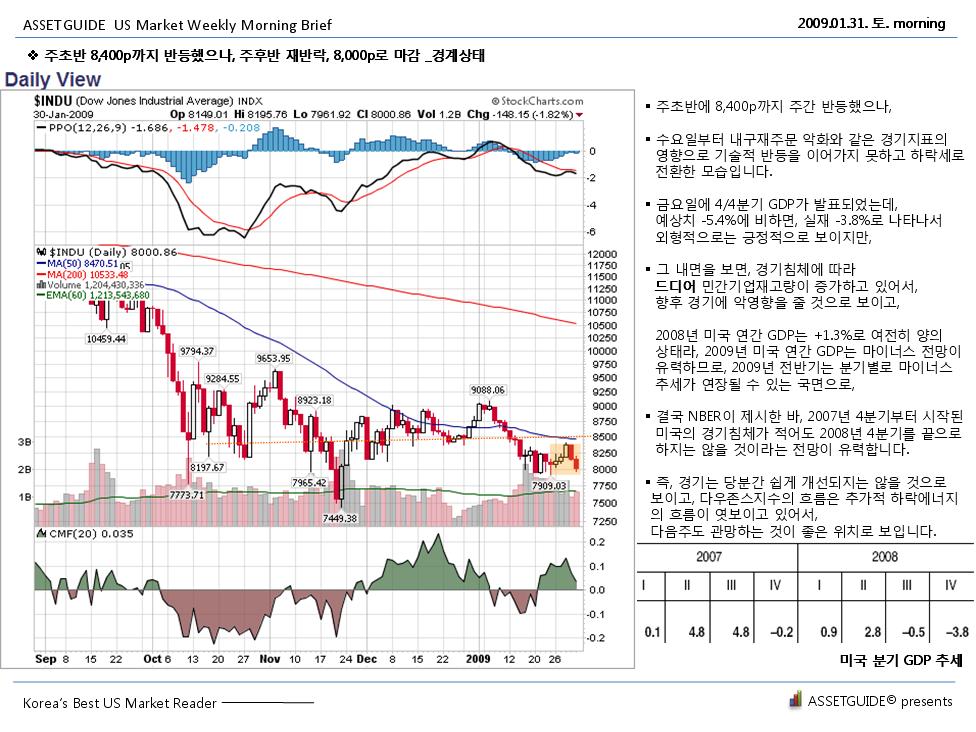

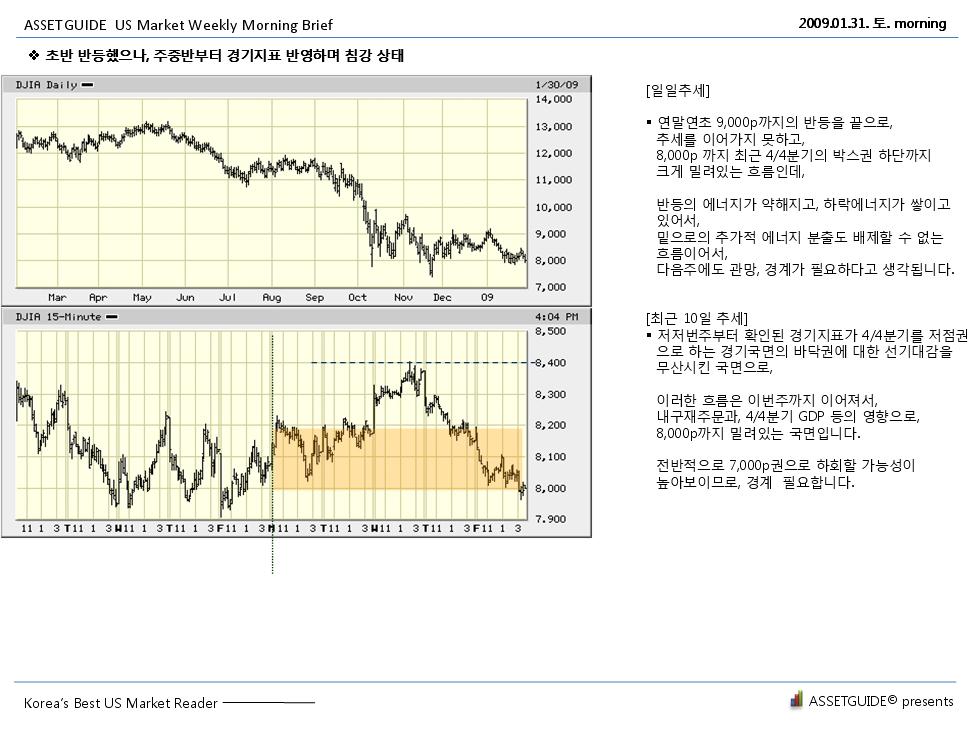

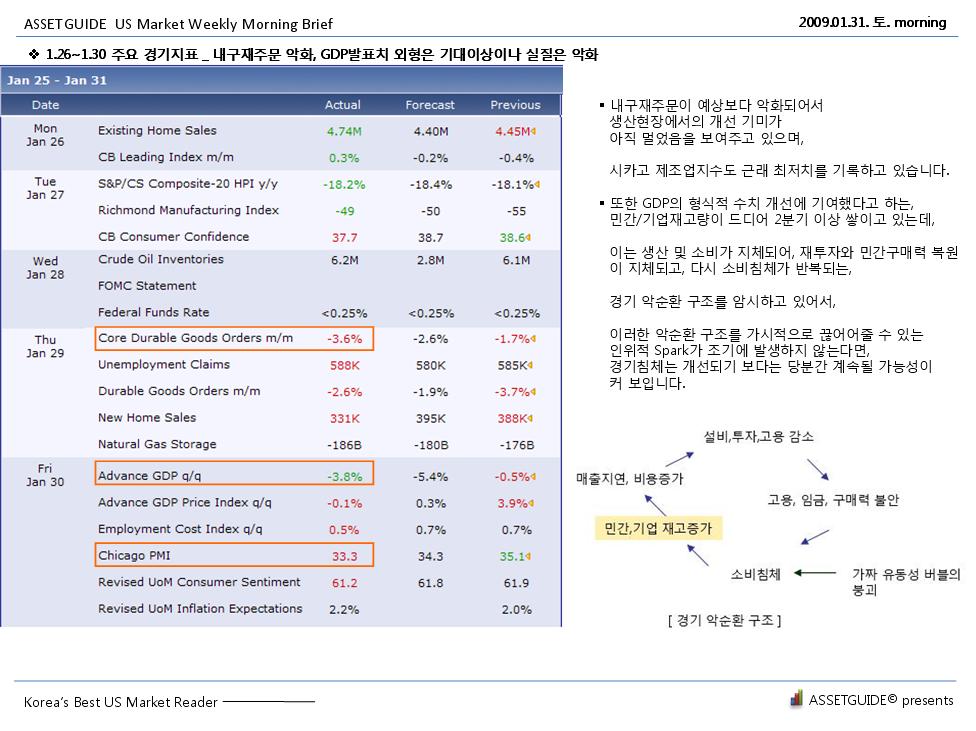

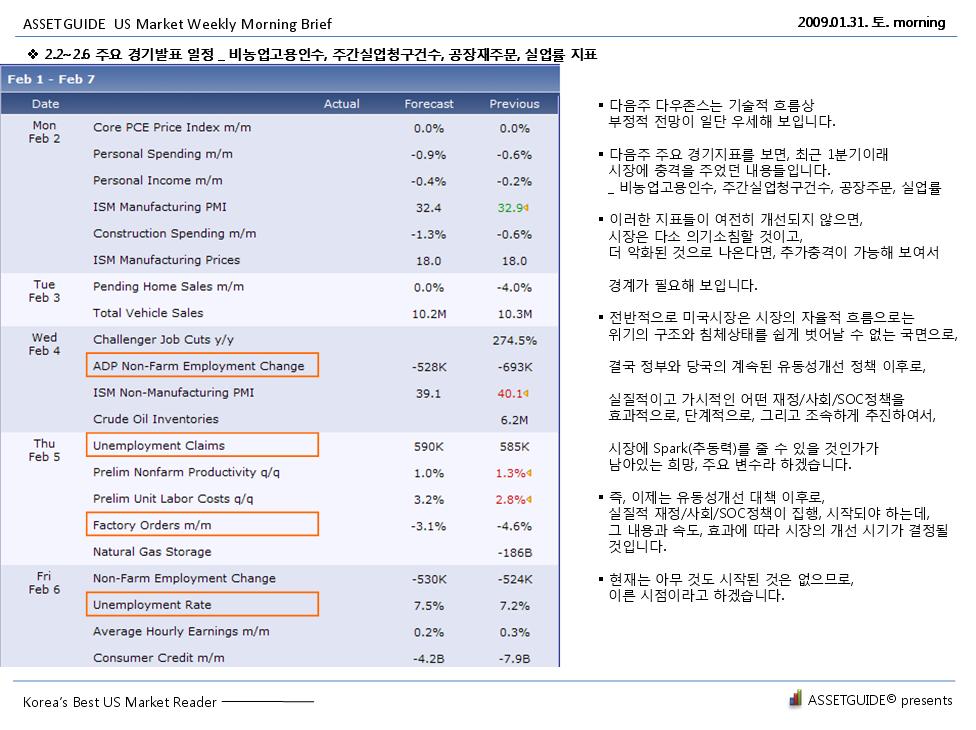

|

|

||||

미국 내구재주문(Durable Goods Orders) 지표가 6월 월간 1.8% 개선된 것으로 나타났습니다.

핵심 내구재주문(Core Durable Goods Orders) 지표는 1.1% 개선되었습니다.

발표 내용에 따르면,

5월 내구재 주문이 1.8% 늘어나서 $1,639억 달러를 기록했는데, 이런 증가폭은 4월 이후 3달째 이어지고 있는 개선세입니다.

교통(transportation)을 제외하면 1.1%, 방위(defense)를 제외하면 1.4% 늘어났습니다.

내구재는 예컨대, 자동차, 컴퓨터, 장치, 항공기처럼, 3년 이상의 수명을 가지는 장주기 제품, 중장비를 말합니다.

미국 내구재주문 (forexfactory.com)

2009년 6월 내구재주문 수치는 예상치 -0.6%(내구재), -0.2%(핵심내구재)에 비해 높게 나타난 것입니다.

그러나, 6월 월간 경제지표, 예컨대 산업생산이나 엠파이어 스테이트 제조업 지수 등은 다시 저조한 흐름도 나타났기 때문에,

기대치를 즉시에 바로 돌리기는 다소 시간이 필요하다고 보이고, 7월 경제지표를 확인해 가야 겠네요.

HIGHLIGHTS FROM THE ADVANCE REPORT ON MANUFACTURERS' SHIPMENTS, INVENTORIES, AND ORDERS

May 2009--------------- Released 8:30 A.M. EDT June 24, 2009

(M3-1(09)-05)

Note: All figures in text are in seasonally adjusted current dollars

For Data - (301) 763-4673

For Questions - Chris Savage or Jessica Young

(301) 763-4832

New Orders

New orders for manufactured durable goods in May increased $2.8 billion or 1.8 percent to $163.9 billion, the U.S. Census Bureau announced today. This was the third increase in the last four months and followed a 1.8 percent April increase. Excluding transportation, new orders increased 1.1 percent. Excluding defense, new orders also increased 1.4 percent.

Shipments

Shipments of manufactured durable goods in May, down ten consecutive months, decreased $3.6 billion or 2.1 percent to $169.9 billion. This was the longest streak of consecutive monthly decreases since the series was first published on a NAICS basis in 1992 and followed a 0.5 percent April decrease.

Unfilled Orders

Unfilled orders for manufactured durable goods in May, down eight consecutive months, decreased $2.0 billion or 0.3 percent to $747.5 billion. This followed a 1.1 percent April decrease.

Inventories

Inventories of manufactured durable goods in May, down five consecutive months, decreased $2.5 billion or 0.8 percent to $323.3 billion. This followed a 1.1 percent April decrease.

Capital Goods Industries

Nondefense

Nondefense new orders for capital goods in May increased $4.9 billion or 10.0 percent to $53.8 billion.

Defense

Defense new orders for capital goods in May increased $0.8 billion or 7.4 percent to $12.0 billion.

Released June 24, 2009. This report presents advance information on two key business indicators: durable goods manufacturers' shipments and orders. Revised and more detailed estimates plus nondurable goods will be published July 2, 2009. The advance report on durable goods for June is scheduled for release July 29, 2009.

Our internet address is: http://www.census.gov/m3

'Market(o)' 카테고리의 다른 글

| 7월 한은 금통위 금리전망 _09.07.08 (0) | 2009.07.08 |

|---|---|

| 2009년 5월 산업활동동향 _경기종합지수,경기동행지수,경기선행지수 _기획재정부 _09.06.30 (0) | 2009.06.30 |

| 미국 FOMC 6월 의사록, 연방 금리 동결 결정 _09.06.24 (0) | 2009.06.25 |

| 세계은행, 세계 경제성장률, 한국 경제성장률 전망 _09.06.22 (0) | 2009.06.23 |

|

| |||||