|

|

||||

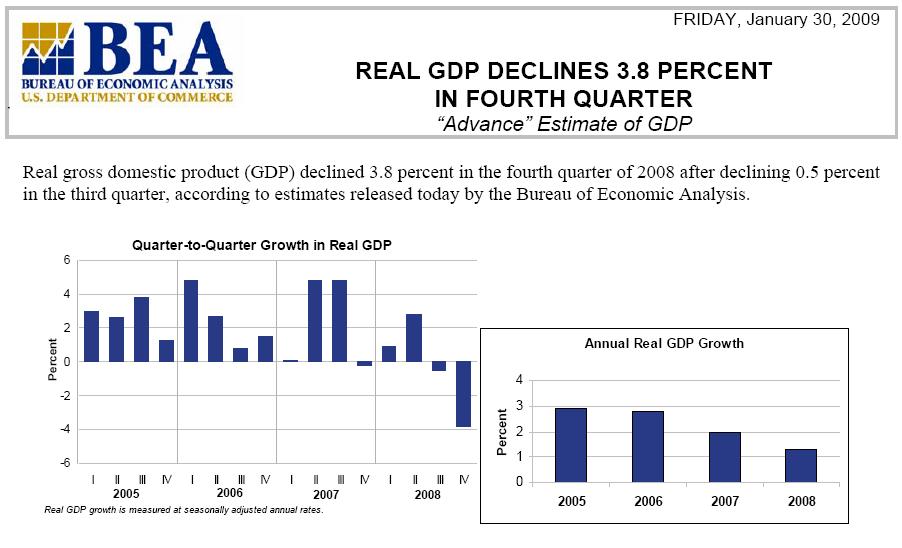

2009년 3분기 미국 GDP, 경제성장률이 +3.5% 상승, 분기 처음으로 양전환(+)하며 예상치를 크게 상회하는 것으로 나타났습니다.

2008년 1분기 최초로 음전환(-)하여 마이너스 성장률을 보이던 미국 분기 GDP 성장률은, 금융위기의 한파 속에, 2009년 2분기까지 하락세를 보였습니다.

2008년 1분기 -0.7%, 2008년 2분기 1.5%에 이어, 2008년 3분기 -2.7%, 4분기 -5.4%, 2009년 1분기 -6.4%, 2분기 -1.0%를 보였습니다.(2005년 미국 GDP 기준)

이러한 하락세 이후의, 2009년 3분기 +3.5% 성장은, 4분기 연속 마이너스 성장률을 벗어나며 최초로 양전환(+)했다는데 큰 의미가 있습니다. 특히 예상치 3.2%를 넘어서는 3.5%의 성장률을 보여주었습니다.

전미경제조사국(NBER)은 2007년 12월부터 미국 경제가 침체에 들어섰다고 선언했기 때문에, 이로부터 2년 이상 경과한 현재시점은 경기사이클이 미약하나마 회복기로 전환될 시점으로 보는 것이 유력합니다. 따라서, NBER 스스로도 조만간 경기침체 종료 선언을 할 가능성이 높습니다.

미국경제분석국(BEA)은 미국 GDP, 경제성장률이 상승한 이유로 다음과 같은 점을 지적했습니다.

- 소비자 소비가 강하게 돌아서고 있다. 새 차와 트럭에 대한 구매가 큰 기여를 했는데, 7-8월에 시행된 연방의 "cash for clunkers" 프로그램(차량교체 프로그램)이 큰 역할을 했다.

- 주택 부문(Housing)이 15분기만에 최초로 돌아섰다.

- 재고투자, 수출, 정부지출이 역시 성장률에 기여했다고 밝혔습니다.

물가 부문을 보면, 3분기에 1.6%, 2분기에 0.5% 상승한 것에 불과하여 안정적이라고 밝혔습니다. 3분기에 다소 높은 것은 에너지 가격 상승만을 반영할 뿐이라고 합니다.

개인소득(Personal Income)은 정부의 사회안전 지원과, 미국 재건 및 재투자법(American Recovery and Reinvestment Act) 조치에 따라 향상되었으나, 이러한 지원 부분을 빼면, 3분기에는 다소 하락하였다고 하네요.

실제로 개인 소득 부분은 2분기 +0.6%에서, 3분기 -0.5%로 하락하였다고 합니다. 그러나 전체 중사이클 추세를 생각할 때, 무난하다고 볼 수 있는 대목입니다. 가처분소득은 전분기 +3.8% 상승에서, 3분기 -3.4% 감소하였으나, 2분기-3분기 전체적으로 보면 중립적인 수준에 있다고 볼 수 있겠습니다.

개인 저축률은 3분기에 3.3%를 기록했고, 2분기는 4.9%였습니다.

금번의 3분기 미국 GDP 추이를 보면, 정부 지출과 지원 프로그램에 따라 물론 예상보다 크게 나온 측면도 있으나, 4분기 연속 하락추세를 종결시키고, 최초로 양전환(+)했다는데 의미가 있습니다.

또한 전분기 -1.0%에서 이번 분기 3.5%로, 상승 전환의 추세가 확실해졌기 때문에, 사실상 미국 경제위기는 종결되었다고 보는 것이 적절한 것으로 생각됩니다.

따라서, 앞으로의 미국경제나 세계경제는 일상적인 사이클과 모멘텀에 따라 추세를 탈 것으로 생각합니다.

그 이전에, 미국 경기사이클의 침체를 선언했던 전미경제조사국(NBER)이 먼저 미국경기 침체의 종료를 공식 선언할 것으로 전망됩니다. 그 시기는 올해 11월이나 12월이 될 것으로 생각되는데, 이는 침체를 선언한 이후 약 2년만의 일이 될 것입니다.

다음은 BEA의 요약 발표 자료입니다.

GDP RISES 3.5 PERCENT IN THIRD QUARTER

Real gross domestic product (GDP) increased 3.5 percent in the third quarter of 2009 after decreasing 0.7

percent in the second quarter, according to estimates from the Bureau of Economic Analysis. The third-quarter

increase was the first since the second quarter of 2008.

Gross Domestic Product

The rise in real GDP reflected the following:

• Consumer spending turned up strongly. Spending on new cars and trucks was a big contributor,

reflecting the federal “cash for clunkers” program, which was in effect in July and August.

• Housing increased for the first time in 15 quarters.

• Inventory investment, exports, and government spending also added to growth.

Prices

Prices of goods and services purchased by U.S. residents increased 1.6 percent in the third quarter after

increasing 0.5 percent in the second quarter, mainly reflecting an upturn in energy prices.

Excluding food and energy, prices rose 0.5 percent after rising 0.8 percent.

Personal Income

In the second quarter, personal income was boosted by government payments to recipients of social security and

other benefits enacted in American Recovery and Reinvestment Act. Coming off those payments, personal

income declined in the third quarter.

Current-dollar personal income fell 0.5 percent after rising 0.6 percent. Real disposable personal income—

income adjusted for inflation and taxes—declined 3.4 percent in the third quarter after increasing 3.8 percent in

the second quarter.

The personal saving rate—personal saving as a percent of current-dollar disposable personal income—was 3.3

percent in the third quarter. In the second quarter, it was 4.9 percent.

gdp3q09_adv_fax.pdf

gdp3q09_adv_fax.pdf출처 : 미국 경제분석국(BEA)

[관련글]

미국 경기침체기의 평균 지속 기간

미국 GDP, 경제성장률 변화 추이 _1995~2009

2009년 3분기 국내 GDP +2.9% 상승 (Korea)

'Market(o)' 카테고리의 다른 글

| FOMC 11월 공개 의사록, 제로금리 계속 유지 _09.11.04 (0) | 2009.11.05 |

|---|---|

| 경기선행지수, 경기동행지수, 경기후행지수 _통계청 3/4분기 산업활동동향 _09.10.30 (0) | 2009.11.04 |

| 2009년 3분기 GDP, 국내총생산, 경제성장률 2.9% 상승 _한국은행 _09.10.26 (0) | 2009.10.26 |

| 베이지북 Beige Book 10월호 _FRB 미국 경제상황 보고 _09.10.21 (0) | 2009.10.22 |

|

| |||||